Deciding when to start claiming Social Security benefits is one of the most significant financial decisions you'll face as you approach retirement. With so many factors to consider, including your age, health, financial needs, and employment plans, the decision can be complex. This guide will explore the key considerations to help you make an informed choice about when to start claiming Social Security.

Understanding Social Security Benefits

Social Security benefits are based on your lifetime earnings, with higher lifetime earnings resulting in larger benefits. You can begin receiving benefits as early as age 62, but the longer you wait—up to age 70—the larger your monthly benefit will be.

- Early Retirement Age (62): The earliest age you can start receiving benefits. However, starting at 62 will reduce your monthly benefit by approximately 25-30%, depending on your full retirement age (FRA).

- Full Retirement Age (FRA): This is the age at which you are entitled to your full Social Security benefit. The FRA varies based on your birth year. For those born in 1960 or later, the FRA is 67.

- Delayed Retirement (up to age 70): If you delay claiming benefits past your FRA, your monthly benefit will increase by about 8% for each year you wait, up to age 70.

Key Factors to Consider

- Life Expectancy

- Impact: Your expected lifespan plays a crucial role in deciding when to start benefits. If you have a longer life expectancy, delaying benefits can result in higher lifetime income. Conversely, if you expect a shorter lifespan, starting benefits earlier might make more sense.

- Considerations: Take into account your health, family history, and lifestyle. While no one can predict the future, understanding your likely lifespan can help guide your decision.

- Financial Needs

- Impact: Your financial situation is another critical factor. If you have sufficient savings, pensions, or other retirement income, you may be able to delay Social Security to maximize benefits. If not, you might need to start benefits earlier.

- Considerations: Evaluate your overall financial health, including retirement savings, debts, living expenses, and other sources of income. If your savings are substantial, delaying benefits could enhance your long-term financial security.

- Employment Status

- Impact: If you plan to work during your early 60s, starting Social Security benefits might not be the best choice due to potential earnings penalties. Benefits claimed before your FRA may be reduced if your earnings exceed certain limits.

- Considerations: If you continue working, especially in a high-paying job, delaying benefits could allow you to avoid reductions and increase your future monthly benefits. However, if you stop working before your FRA, starting benefits earlier might be necessary to cover expenses.

- Spousal and Survivor Benefits

- Impact: If you are married, your decision will also impact your spouse’s benefits. A higher earner delaying benefits can increase the survivor benefits for the lower-earning spouse.

- Considerations: Couples should coordinate their claiming strategies to maximize their combined benefits. For example, one spouse may start benefits early while the other delays, balancing the need for immediate income with long-term benefit maximization.

- Longevity of Benefits

- Impact: The age you start claiming Social Security will affect how long you receive benefits and the total amount over your lifetime. Starting early results in smaller monthly checks over a longer period, while delaying results in larger checks over a shorter period.

- Considerations: If you start at 62, you will receive benefits for a longer time, but each payment will be smaller. If you delay until 70, you’ll receive larger payments, but for a shorter period. The break-even point, where the total benefits received would be equal whether you started at 62 or 70, generally occurs around age 80-85.

- Inflation and Cost-of-Living Adjustments (COLA)

- Impact: Social Security benefits are adjusted annually for inflation. Starting benefits later can result in higher base payments, which will increase more significantly with future COLA adjustments.

- Considerations: A higher initial benefit, due to delaying, means future COLA increases will be based on a larger amount, potentially offering better protection against inflation in the long run.

Scenarios to Illustrate the Decision

- Early Retirement with Limited Savings:

- Profile: Age 62, modest savings, health concerns, no other significant income.

- Decision: Starting Social Security at 62 might be the best choice to provide necessary income, despite the reduced monthly benefit.

- Working Past Full Retirement Age:

- Profile: Age 67, still employed, good health, sufficient retirement savings.

- Decision: Delaying benefits until 70 could maximize lifetime income and increase the spousal benefit, given continued employment and financial stability.

- Married Couple with Disparate Earnings:

- Profile: One spouse is 62, lower earner; the other is 67, higher earner.

- Decision: The lower earner might start benefits at 62, while the higher earner delays until 70, optimizing both the immediate and future financial security.

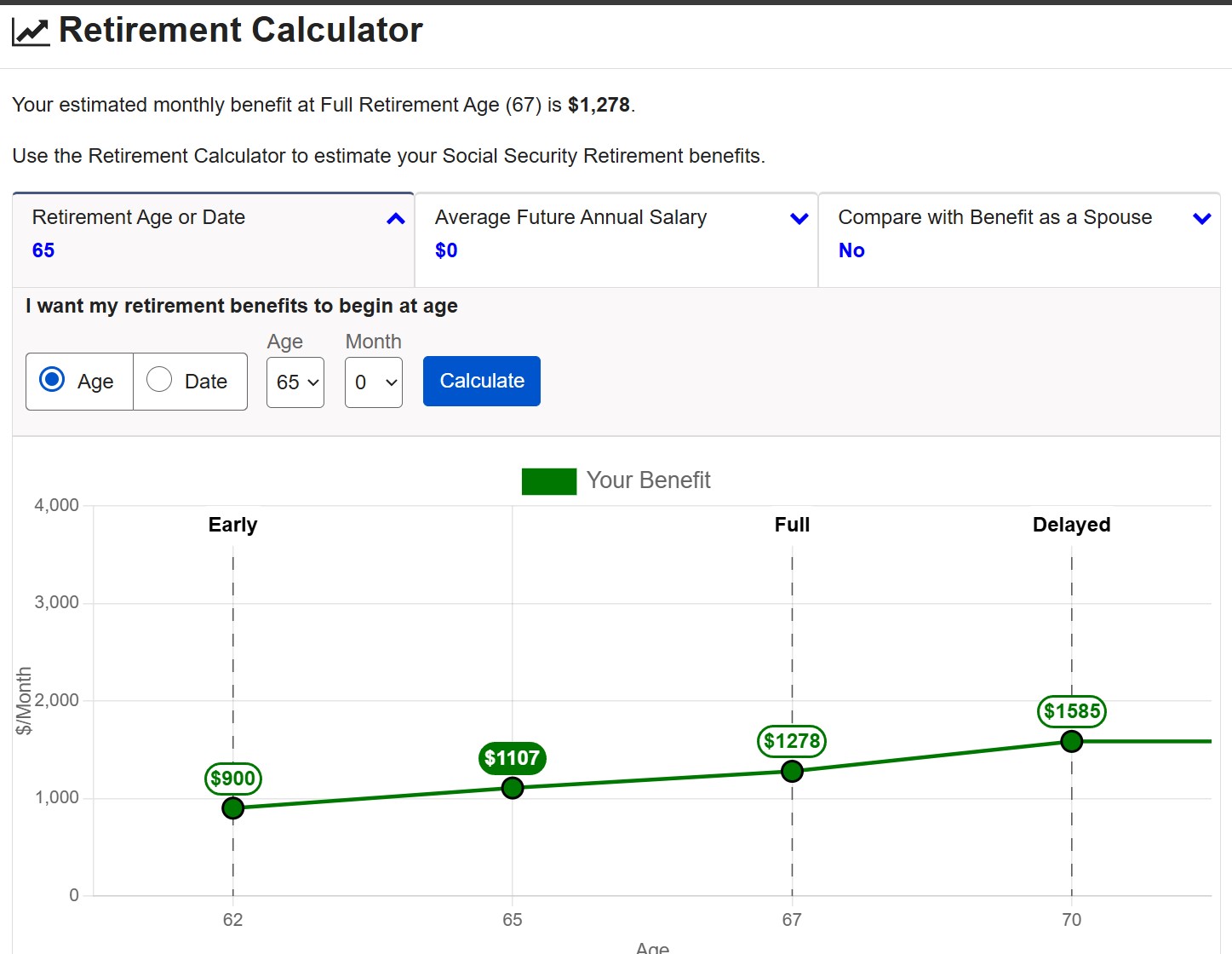

Finding Your Numbers

The Social Security Administration has a website at ssa.gov. Once you create an account using you social security number you will be able to see your data based on your work history. There is even a retirement calculator on the site. It starts out with three early full and delayed corresponding to age 62, 67 and 72 for most people. You can also plug in s retirement age and it will show the monthly benifit based on that age. for example 65 and 0 months would give a different number.

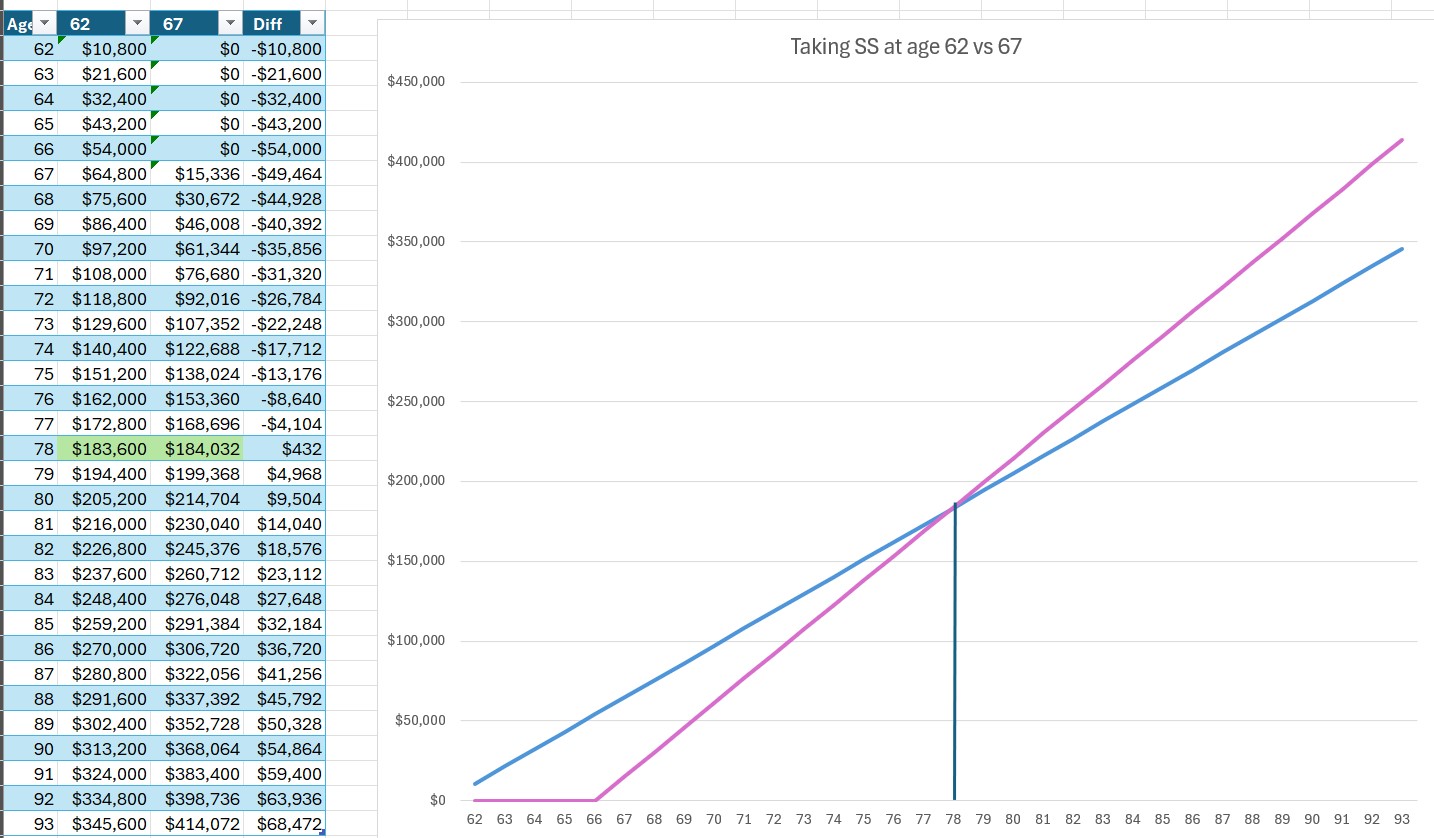

Charting the difference claiming at 62 vs 67

You can claim at any time after your 62 birthday. This chart would be different fo rage 63 vs 67 or 64 vs 67 however one thing that is similar is that in each case the break even point is around 78 years old. You can see then since you did not collect your benefit for the first five years, collecting puts you ahead until you are almost 78 years old. This does not count investing the money you took in the first five years. if you dollar cost averaged that money into a safe bond investment at 5% or the S&P which averaged 10.5% since 1926 that crossover would move significantly further than 78.

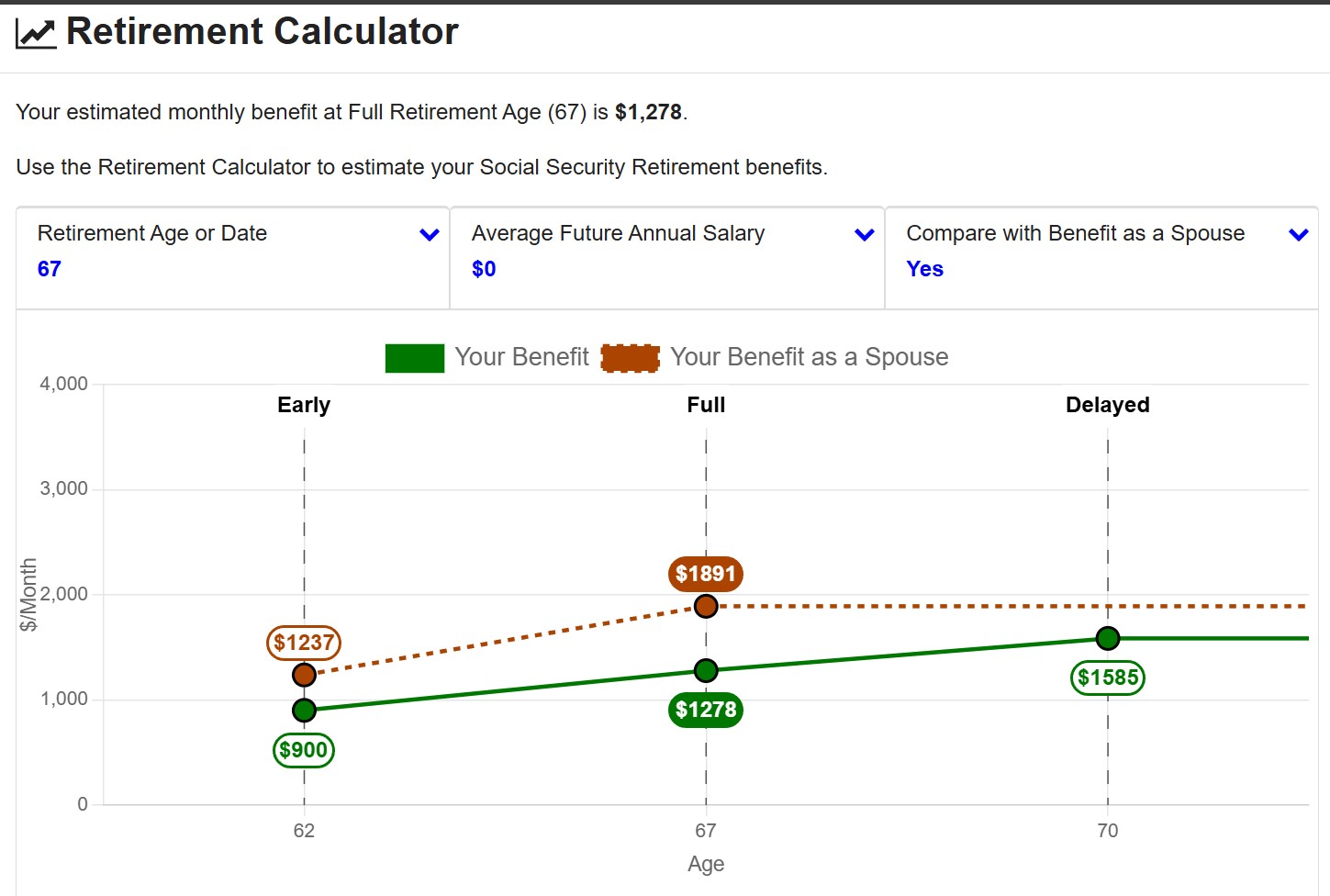

Spousal Benefits

If you spouse made more than you as you may have spent years raising the children you can claim spousal benefits. This is calculated at half of your spouses benefit rate based on their full retirement. The calculator allows you to compare your benefit to spousal benefits. When collecting spousal benefits, the calculated benefit does not increase after full retirement age so it would not make sense to wait any longer. IN the scenario below it is obvious that collecting spousal benefits is the wat to go.

One other thing to be aware of. If your spouse starts collecting early it does not affect yout benefit. You still collect based on their full retirement amount if you wait until full retirement.

Conclusion

The decision of when to start claiming Social Security benefits is deeply personal and should be based on a careful analysis of your unique circumstances. Consider your life expectancy, financial needs, employment plans, and the impact on spousal and survivor benefits.

While starting early offers the advantage of immediate income, delaying benefits can provide greater financial security in your later years. Consulting with a financial advisor can help you weigh these factors and create a strategy that aligns with your long-term retirement goals. By understanding the trade-offs, you can make a more informed decision that best supports your retirement lifestyle.