Medicare is a federal health insurance program primarily for people aged 65 and older, but it also covers certain younger individuals with disabilities and those with End-Stage Renal Disease. Navigating the Medicare landscape can be complex due to the variety of plan options, coverage levels, and associated costs. This guide aims to clarify the basics of Medicare, the different plan options available, and the considerations for choosing between a standard Medicare plan and a Medicare Advantage plan. Additionally, we'll explore the role of Medicare specialists and how to work with them effectively.

The Basics of Medicare: Understanding the Plans by Letter

Medicare is divided into several parts, each offering different types of coverage. These are commonly referred to by letters: Part A, Part B, Part C, and Part D, as well as Medicare Supplement (Medigap) plans, which are also identified by letters.

Medicare Part A (Hospital Insurance)

- Coverage: Part A covers inpatient hospital care, skilled nursing facility care, hospice care, and some home health care.

- Deductibles: The deductible for Part A in 2024 is $1,632 per benefit period. There are also coinsurance costs that vary based on the length of your hospital stay.

- Pros: Part A is generally premium-free if you or your spouse paid Medicare taxes for at least 10 years.

- Cons: Out-of-pocket costs can be high if you require extended hospital or skilled nursing facility stays.

Medicare Part B (Medical Insurance)

- Coverage: Part B covers outpatient care, doctor visits, preventive services, durable medical equipment, and some home health care.

- Deductibles: The annual deductible for Part B in 2024 is $240. After the deductible is met, you typically pay 20% of the Medicare-approved amount for most services.

- Pros: Part B covers a wide range of medically necessary services.

- Cons: Premiums are required, which are based on your income. Higher-income individuals pay more.

Medicare Part C (Medicare Advantage)

- Coverage: Part C is an alternative to Original Medicare and is offered by private insurance companies. It includes Part A, Part B, and usually Part D (prescription drug coverage), as well as additional benefits like vision, dental, and hearing.

- Deductibles: Deductibles and out-of-pocket costs vary widely depending on the specific plan.

- Pros: Medicare Advantage plans often offer extra benefits not covered by Original Medicare, and some plans have low or no additional premiums.

- Cons: You may be limited to a network of providers, and there may be more restrictions on when and where you can receive care.

Medicare Part D (Prescription Drug Coverage)

- Coverage: Part D provides prescription drug coverage. Plans are offered by private insurers and vary in terms of the drugs covered.

- Deductibles: The maximum deductible for Part D in 2024 is $545, though some plans may have lower or no deductibles.

- Pros: Helps cover the cost of prescription drugs, which can be a significant out-of-pocket expense.

- Cons: You may face a coverage gap (donut hole) where you pay a higher share of drug costs until you reach catastrophic coverage.

Medigap Plans

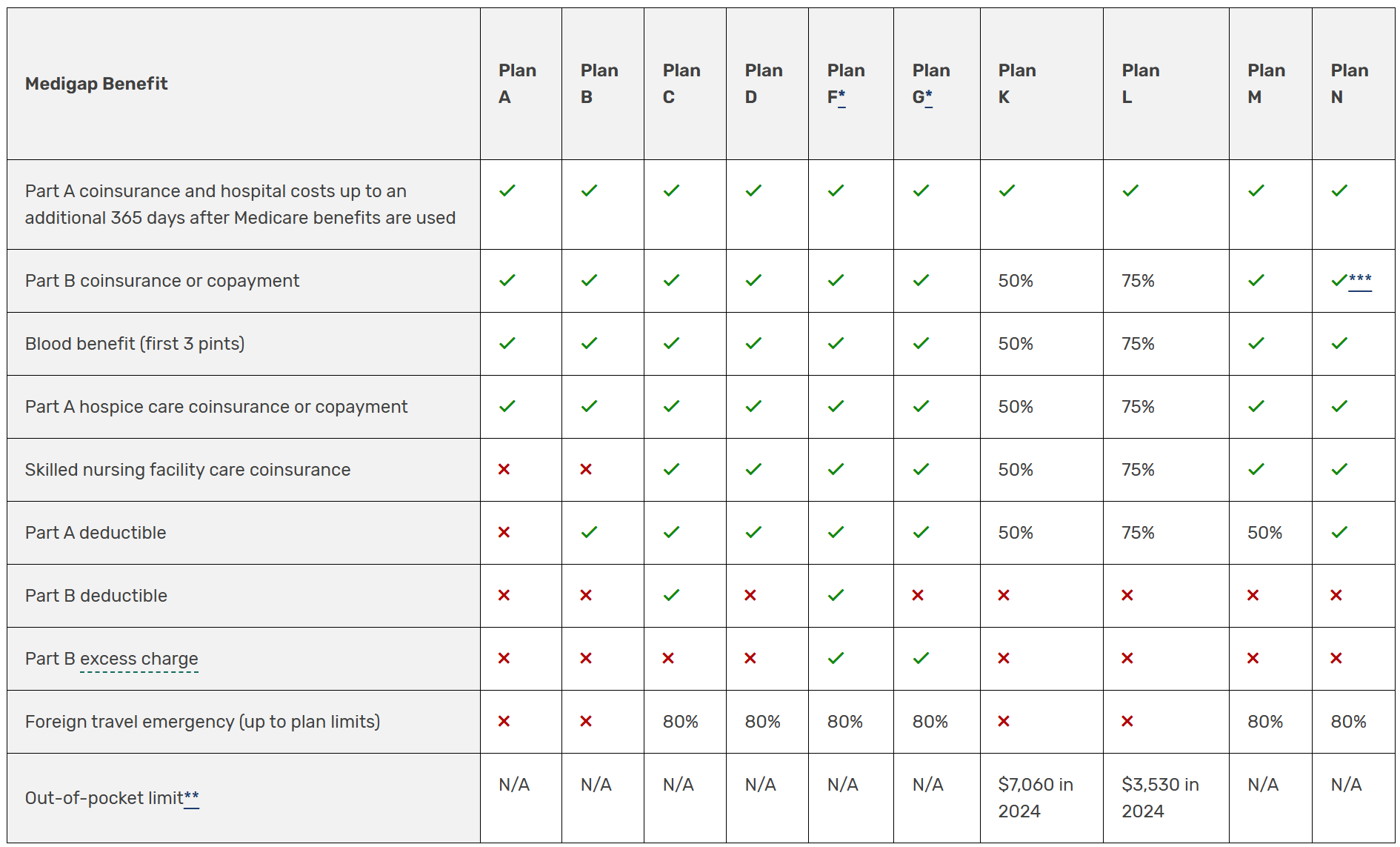

Medigap plans, also known as Medicare Supplement Insurance, help cover out-of-pocket costs that Original Medicare (Part A and Part B) doesn't, such as copayments, coinsurance, and deductibles. Medigap plans are standardized and labeled by letters and while each lettered plan offers different levels of coverage, the benefits for each plan are the same regardless of the insurance provider.

Medicare Plan G

Medigap Plan G is one of the most popular and comprehensive Medicare Supplement Insurance plans available.

- Coverage: It covers nearly all out-of-pocket costs that Original Medicare (Part A and Part B) does not, making it a favorite among those seeking broad coverage. It does not cover the Medicare Part B deductible.

- Pros:

- Comprehensive Coverage: Plan G covers almost everything except the Part B deductible, which makes it a near-total solution for those looking to minimize out-of-pocket healthcare costs.

- Coverage for Excess Charges: It is one of the few plans that covers Medicare Part B excess charges, which can be a significant cost if your provider charges more than Medicare's approved amount.

- No Need for Copays: Unlike some other plans, such as Plan N, Plan G does not require copayments for doctor visits or emergency room visits.

- Predictability: With Plan G, your costs are predictable since nearly all services are covered after you meet the Part B deductible.

- Cons:

- Part B deductible Does not cover the Part B deductible, so enrollees must pay this out-of-pocket.

- Higher Premiums: Since it offers broad coverage, Plan G typically comes with higher monthly premiums compared to less comprehensive Medigap plans.

- Foreign Travel Emergency Coverage Limitations: While it does cover emergency care abroad, the coverage is limited to 80% and has maximum limits.

- Who Should Consider Plan G?

- New Medicare Beneficiaries: If you became eligible for Medicare after January 1, 2020, and Plan F is no longer available to you, Plan G is the next best option for comprehensive coverage.

- Frequent Medical Service Users: Those who expect to frequently use healthcare services and want minimal out-of-pocket costs may benefit from the extensive coverage of Plan G.

- Travelers: If you travel internationally, the foreign travel emergency coverage might appeal to you.

- People Concerned About Excess Charges: Since it covers Medicare Part B excess charges, Plan G is a good choice for individuals who see providers who may charge more than the Medicare-approved amount.

Medicare Plan K

Medigap Plan K is one of the Medicare Supplement Insurance plans that provides partial coverage for certain out-of-pocket costs that Original Medicare (Parts A and B) doesn't cover. Plan K is unique among the Medigap plans because it only covers a portion of certain costs (50%) and includes an out-of-pocket limit, which offers financial protection once you've reached that cap.

- Coverage: Covers 50% of some services, such as Medicare Part B copayments, Part A hospice care, skilled nursing facility coinsurance, and Part A deductible. It has an out-of-pocket limit, after which it covers 100% of Medicare-covered services.

- Pros:

- Lower Premiums: Plan K generally has lower monthly premiums compared to other Medigap plans because it only covers 50% of many costs.

- Out-of-Pocket Protection: The out-of-pocket maximum provides financial security by capping your annual expenses. Once you hit that cap, your plan covers all Medicare-approved costs.

- Basic Coverage: Plan K provides essential coverage, including hospital coinsurance and skilled nursing care coinsurance, which can help with significant healthcare costs.

- Cons:

- Partial Coverage: Plan K only covers 50% of most costs, which means you'll still be responsible for half of the expenses for services like doctor visits, blood, and hospice care.

- No Part B Excess Charges Coverage: Plan K does not cover Part B excess charges, which are costs that may arise if your healthcare provider charges more than the Medicare-approved amount for services.

- Higher Out-of-Pocket Costs: Although the premiums are lower, you could end up with higher out-of-pocket costs due to the partial coverage and the need to meet the out-of-pocket maximum before full coverage kicks in.

- Who Might Benefit from Plan K?

- Budget-Conscious Individuals: If you're looking for a Medigap plan with a lower premium and are comfortable with partial coverage and the possibility of higher out-of-pocket costs, Plan K could be a good fit.

- Those Seeking Financial Protection: The out-of-pocket maximum can be appealing if you're concerned about the potential for high medical expenses but don't want to pay high monthly premiums.

Medicare Plan L

Medigap Plan L is a Medicare Supplement Insurance plan designed to help cover some of the out-of-pocket costs that Original Medicare (Part A and Part B) doesn't cover. It offers partial coverage for several services and includes a unique feature: an annual out-of-pocket limit. Once this limit is reached, the plan covers 100% of Medicare-covered services for the rest of the calendar year.

- Coverage: Covers 75% of some services, including Part B copayments, Part A hospice care, skilled nursing facility coinsurance, and the Part A deductible. It also has an out-of-pocket limit.

- Pros:

- Higher coverage than Plan K with a still relatively low premium.

- Out-of-pocket maximum provides financial security.

- Cons:

- Still requires beneficiaries to pay 25% of certain costs.

- Does not cover Part B excess charges.

- Who Should Consider Plan L?

- Medigap Plan L is a good option for Medicare beneficiaries who want some financial protection against high out-of-pocket costs but are comfortable with sharing some costs to keep premiums lower. The out-of-pocket limit is especially appealing to those who worry about the potential for high medical bills in a given year but don't need the comprehensive coverage offered by plans like Plan G.

- It’s important to evaluate your medical needs and financial situation when considering Plan L to ensure it aligns with your healthcare and budgetary goals.

Medicare Plan M

- Coverage: Covers 50% of the Medicare Part A deductible and all other basic benefits. Does not cover the Medicare Part B deductible or excess charges.

- Pros:

- Lower premiums: Because Plan L only provides partial coverage for many services, it tends to have lower premiums compared to more comprehensive plans like Plan F or Plan G.

- Out-of-pocket protection: The annual out-of-pocket limit ensures that you won’t face unlimited expenses in a given year, providing financial security if you require extensive medical care.

- Partial coverage for key services: Plan L provides 75% coverage for many services, which can significantly reduce your out-of-pocket costs compared to having no supplement plan.

Cons:

- Partial coverage: Since Plan L only covers 75% of many services, you'll still be responsible for 25% of these costs. This can add up, particularly if you have frequent medical needs.

- No coverage for Part B excess charges: If your doctor charges more than what Medicare approves, you will be responsible for the difference, as Plan L does not cover these excess charges.

- No foreign travel emergency coverage: If you plan to travel abroad, you'll need to consider additional coverage, as Plan L does not include emergency care outside the United States.

Medicare Plan N

Medigap Plan N is a popular Medicare Supplement Insurance option that offers a good balance of coverage and affordability. It is designed for beneficiaries who want comprehensive coverage without the higher premiums associated with more extensive plans like Plan G or the discontinued Plan F.

- Coverage: Similar to Plan G but requires copayments for some office visits and emergency room visits. Does not cover Medicare Part B excess charges.

- Pros:

- Lower premiums: Plan N typically has lower monthly premiums than more comprehensive plans like Plan G because it shifts some of the costs (e.g., copayments) to the beneficiary.

- Broad coverage: Plan N provides extensive coverage for hospital stays, skilled nursing care, and many of the costs associated with Medicare Part A and B.

- Cost control: Though it requires some out-of-pocket payments, Plan N still significantly reduces the overall financial burden compared to relying solely on Original Medicare.

- Cons:

- Copayments: While relatively small, copayments for office and emergency room visits can add up over time, especially if you require frequent care.

- No Part B excess charges coverage: If you visit a doctor who charges more than the Medicare-approved amount, you’ll be responsible for the excess charges.

- No Part B deductible coverage: You will need to pay the Part B deductible out-of-pocket each year.

- Who Should Consider Plan N

- Healthy individuals: Plan N is well-suited for beneficiaries who do not expect frequent doctor visits or medical services, as the copayments will be minimal for them.

- Budget-conscious seniors: It’s a good option for those who want a balance of comprehensive coverage and lower premiums but are willing to pay some out-of-pocket costs as needed.

- Overall, Medigap Plan N is a solid choice for those looking to save on premiums while still receiving robust coverage for many of Medicare's gaps, with a few manageable out-of-pocket costs.

Medicare Advantage vs. Original Medicare: Pros and Cons

When choosing between Medicare Advantage (Part C) and Original Medicare (Part A and Part B), it’s essential to weigh the pros and cons to determine which option best suits your needs.

Original Medicare

Pros:

- Flexibility: You can see any doctor or specialist who accepts Medicare, without needing a referral.

- No Network Restrictions: You have nationwide coverage without network restrictions.

Cons:

- Out-of-Pocket Costs: Without supplemental insurance, you could face significant out-of-pocket costs for deductibles, copayments, and coinsurance.

- Limited Coverage: Does not cover routine dental, vision, or hearing care, and lacks additional benefits that Medicare Advantage plans might offer.

Medicare Advantage (Part C)

Pros:

- Comprehensive Coverage: Often includes extra benefits like dental, vision, hearing, and wellness programs.

- One-Stop-Shop: Combines Medicare Part A, Part B, and usually Part D into one plan.

- Lower Out-of-Pocket Costs: Many plans have lower out-of-pocket costs compared to Original Medicare.

Cons:

- Network Restrictions: You may be limited to a network of doctors and hospitals, which can restrict your choice of providers.

- Referrals Required: Some plans require referrals to see specialists.

- Potential Higher Costs for Out-of-Network Care: If you need care outside the plan’s network, it could be more expensive.

Making the Right Choice and Challenges to Making Changes Later

There can be issues when trying to change your Medicare plan at a later time. Here are some key considerations:

Enrollment Periods

Medicare has specific enrollment periods during which you can make changes to your plan. Outside of these periods, switching plans may not be possible unless you qualify for a special enrollment period (SEP). The key periods are:

- Initial Enrollment Period (IEP): When you first become eligible for Medicare.

- Annual Enrollment Period (AEP): From October 15 to December 7 each year, during which you can make changes to your Medicare Advantage (Part C) or Medicare prescription drug (Part D) plan.

- Medicare Advantage Open Enrollment Period: From January 1 to March 31, you can switch Medicare Advantage plans or return to Original Medicare.

Medical Underwriting for Medigap Plans

If you're enrolled in a Medigap (Medicare Supplement) plan and wish to switch to a different Medigap plan after your initial enrollment, you may be subject to medical underwriting. This means insurers can evaluate your health and potentially charge higher premiums, limit coverage, or deny you coverage based on pre-existing conditions. However, during your initial Medigap enrollment or if you qualify for a guaranteed issue right, you cannot be denied coverage or charged more due to health conditions.

Plan Availability and Changes

Plans can change each year, including benefits, premiums, and networks. If your plan changes, you may need to review and switch during the AEP to maintain the coverage that best suits your needs. Additionally, not all plans are available in all areas, so moving to a new location could limit your options for switching.

Prescription Drug Coverage (Part D)

If you switch Part D plans, ensure your new plan covers your medications. Formularies (the list of covered drugs) vary between plans, and switching could result in your medications no longer being covered or being covered at a higher cost.

Network Restrictions

If you are in a Medicare Advantage plan, be aware that these plans often have networks of doctors and hospitals. Switching plans could mean that your current healthcare providers are no longer in-network, potentially increasing your costs or requiring you to find new providers.

Potential Penalties

Delaying enrollment in Part D or not maintaining creditable prescription drug coverage can result in a late enrollment penalty if you try to enroll in a Part D plan later. This penalty is permanent and added to your monthly premium.

Changing your Medicare plan later can be done, but it requires careful consideration of timing, plan availability, and potential costs.

Working with a Medicare Specialist

Navigating Medicare can be challenging, and working with a Medicare specialist can help you make informed decisions. Specialists can guide you through the plan selection process, ensuring that you choose coverage that meets your needs.

Types of Medicare Specialists

- Independent Agents: These specialists work with multiple insurance carriers and can offer you a range of plan options. They are typically unbiased and can help you compare different plans to find the best fit.

- Captive Agents: These agents work for a specific insurance company and can only offer plans from that company. While they may provide deep knowledge of the company's offerings, they may not offer the broadest range of choices.

- Brokers: Medicare brokers are similar to independent agents but may have access to a wider range of plans. They can provide more extensive comparisons across different insurers.

- Medicare Consultants: Consultants do not sell insurance but provide advice on choosing the right Medicare plan. They charge a fee for their services and may offer a more in-depth analysis of your needs.

Cautions When Working with a Medicare Specialist

- Beware of High-Pressure Sales Tactics: Some agents may use high-pressure tactics to push you toward a plan that may not be the best fit for you. Always take your time to review your options and make an informed decision.

- Verify Credentials: Ensure the specialist is licensed and has a good reputation. You can check their credentials through your state’s insurance department.

- Understand the Compensation Structure: Ask how the specialist is compensated. Agents and brokers typically earn commissions from insurance companies, which could influence the plans they recommend.

- Be Aware of Plan Changes: Medicare plans can change annually. A good specialist will help you review your plan each year to ensure it still meets your needs.

From medicare.gov

Note: Plan C & Plan F aren’t available if you turned 65 on or after January 1, 2020, and to some people under age 65. You might be able to get these plans if you were eligible for Medicare before January 1, 2020, but not yet enrolled. Learn more about who can buy this plan.

*Plans F & G offer a high deductible plan in some states.

**Plans K & L show how much they'll pay for approved services before you meet your out-of-pocket yearly limit and Part B deductible. After you meet them, the plan will pay 100% of your costs for approved services.

***Plan N pays 100% of the costs of Part B services, except for copayments for some office visits and some emergency room visits.

Understanding Medicare and selecting the right plan can significantly impact your healthcare experience and financial well-being. By familiarizing yourself with the different parts of Medicare, considering the pros and cons of Medicare Advantage versus Original Medicare, and working with a qualified Medicare specialist, you can make informed decisions that align with your healthcare needs and financial situation.

Remember, Medicare is not a one-size-fits-all program. Regularly reviewing your coverage, staying informed about changes, and seeking expert advice when needed can help you navigate Medicare with confidence.